Intrigued by the resurgence of adjustable-rate mortgages (ARMs)? Join us in deciphering this trend and discover why it's a far cry from the past. Let's unravel the intriguing narrative of how ARMs are making a smart return to the real estate arena.

Why ARMs Are Staging a Comeback

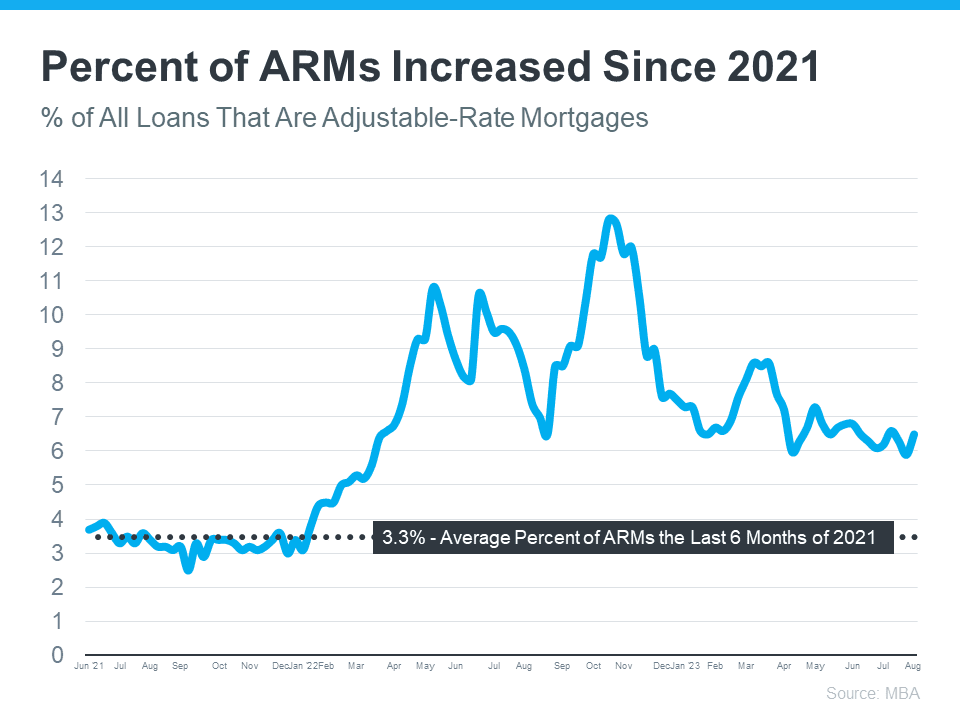

Venture into the realm of mortgage dynamics as we dissect the data presented by the Mortgage Bankers Association (MBA). This graph portrays the upward trajectory of adjustable-rate mortgages over recent years.

Witness the transformation: From constituting a modest 3% of all mortgages in 2021, ARMs have experienced a remarkable revival in the previous year. But why this sudden surge? The answer is a dance between interest rates and borrower preferences.

The ARMs of Today vs. Their Predecessors

Before you jump to conclusions, let's clear the air. Today's ARMs stand worlds apart from their counterparts of the pre-2008 era. The housing crash taught us invaluable lessons, primarily about the perils of lax lending standards. Back then, ARM recipients could secure loans without substantiating their income, employment, or assets. In essence, loans were extended to individuals who wouldn't have qualified under stricter criteria, leading to a crisis.

Fast forward to today, and the landscape is transformed. Lenders have adopted a more stringent approach, demanding evidence of income, assets, and employment. The echoes of the past guide present-day lending, emphasizing loan qualification and the borrower's capacity to repay.

Archana Pradhan, Economist at CoreLogic, eloquently highlights the shift:

“Around 60% of Adjustable-Rate Mortgages (ARM) that were originated in 2007 were low- or no-documentation loans . . . Similarly, in 2005, 29% of ARM borrowers had credit scores below 640 . . . Currently, almost all conventional loans, including both ARMs and Fixed-Rate Mortgages, require full documentation, are amortized, and are made to borrowers with credit scores above 640.”

In essence, Laurie Goodman at Urban Institute encapsulates the shift:

“Today’s Adjustable-Rate Mortgages are no riskier than other mortgage products and their lower monthly payments could increase access to homeownership for more potential buyers.”

Embrace the New Era

So, if you're harboring concerns that today's ARMs mirror the housing crash, breathe easy. The playbook has changed, ensuring a safer and smarter approach.

And if you're a first-time homebuyer, our guidance is at your fingertips. Discover lending options that navigate today's affordability challenges with ease. Reach out to our trusted lenders and embark on your homeownership journey with confidence.